|

|

|

|||

Department of Agriculture and Food Systems

|

||||

|

||||

|

|

|

|||

Department of Agriculture and Food Systems

|

||||

|

||||

|

|

Agribusiness Review - Vol. 12 - 2004Paper 5 AGRICULTURAL PROCESSING AND THE WA ECONOMY: A GENERAL EQUILIBRIUM ANALYSISPeter Johnson and Nazrul Islam [1] Peter Johnson, Economic Research Centre, University of Western Australia . ABSTRACTThis paper investigates the impact of an expansion in agricultural processing on the Western Australian economy by modifying and applying a Computable General Equilibrium (CGE) economic model of Western Australia (called WAM). WAM was used to simulate the effects of a $1 million expansion in eight agricultural processing industries. The results show that there is a range of positive impacts from agricultural processing. On average, a $1 million expansion in agricultural processing is estimated to increase the State's GSP (Gross State Product) by $649,000, and total output by $1.9 million. The expansion of the Wine and spirits industry is estimated to have the largest impact while the Textile fibres, yarns and woven fabrics industry has the smallest impact on the Western Australian economy. 1. IntroductionWith its favourable factor endowments, Western Australia enjoys a comparative advantage in agricultural production and export. The State produces a wide range of export oriented agricultural commodities, including, broadacre crops (predominantly wheat), wool, sheep, cattle and other livestock. In 1998/99, the gross value of agricultural production in WA stood at $4.9 billion [2] , which represents about 15 per cent of national production. During the past two decades, the agricultural sector in WA grew at an average rate of over 6 per cent per annum (Islam, 2000). However, although WA is a major producer of agricultural commodities, and has a wealth of natural advantages including a clean environment and a stable and strong economy, not much agriculture-based processing has taken place in the State. This is in spite of the fact that for a long time an important policy objective of the WA government has been to expand the local processing of primary products before export. This policy is in place because it is believed that downstream processing is important for ensuring the continued growth of WA agriculture. While accounting for around 15 per cent of Australia 's primary agricultural output, WA produces only about 7 per cent of the gross product of the national food manufacturing industry (ABS, 2001a and 2001b). So, while about 75 per cent of WA's agricultural output is exported, it is mostly in unprocessed form. Between 1995 and 1999, on average, only about 12 per cent of the total WA agricultural exports were in processed form. By comparison, over 50 per cent of the agricultural exports from the rest of Australia were in processed form. For some individual commodities, the lack of processing in WA is even worse. For example, WA accounts for only 4 per cent of the national exports of meat products, while its share in national live animal exports is over 40 per cent. Australia as a whole lags behind other exporters of agricultural processed commodities [3] and WA clearly lags behind the rest of Australia in agricultural processing activities. Given the marked differences between the prices of processed agricultural products and unprocessed agricultural commodities, one might suspect that the WA economy is losing heavily by not processing its primary products before export. With market access improving (due to multilateral trade negotiations under the auspices of GATT/WTO and APEC) and with growing demand for processed foods, the prospect for downstream processing of primary products in WA has improved. At the federal level, the government has adopted a number of programs and initiatives to improve the international competitiveness and export orientation of the agricultural processing industries (see, e.g., National Food Industry Strategy report, AFFA, 2002). With WA's low level of agricultural processing, the State is failing to take advantage of these opportunities. To appreciate the contribution that expanded agricultural industries may have on the WA economy, in this paper we simulate the impact of a $1 million expansion in a variety of agricultural processing industries. This is accomplished using a Computable General Equilibrium (CGE) model of the Western Australian economy. This model helps us to obtain answers to the following questions:

The remainder of this paper is divided into four sections. Section 2 provides an overview of the agricultural and agricultural processing industries in WA. In Section 3, the characteristics of the CGE model for the WA economy is described, while in Section 4, the model is applied and its results are discussed in detail. Finally, Section 5 concludes the paper and presents a summary of the major findings. 2. FOOD AND AGRICULTURAL PROCESSING IN WESTERN AUSTRALIAAlthough the agriculture sector is relatively important to the WA economy, contributing more than four per cent to the State's GSP [compared to less than three per cent for the rest of Australia (ROA) (ABS, 2001)], the State's food processing sector accounts for a little more that one per cent of the State's GSP, as compared to about three per cent for the ROA (Islam and Johnson, 2003). [4] The relative lack of food processing in WA is in part a reflection of the State's relatively low share of Australian manufacturing. As can be seen in Table 2.1, WA's share of the national food manufacturing value-added in only 6.5 per cent (see column 3), while its share of total manufacturing value-added is only 7.4 per cent (see column 5). However, WA also ranks the lowest amongst the Australian States in terms of food manufacturing share (18 per cent) of total manufacturing (see column 6 of Table 2.2), indicating that the lack of food processing in the State is due to more than just WA's relatively small manufacturing base. Table 2.1. Food 1 manufacturing value added in Australian States, 1999/2000

Notes: Notes:

Source: ABS (2001a and 2001b) A detailed look at the extent to which WA agricultural commodities are processed and exported is presented in Table 2.2. As can be seen in row 7, only 25 per cent (14 + 11 per cent, see columns 3 and 5) of the State's primary agricultural commodities are processed in some form or other. The remaining 75 per cent is marketed in raw commodity form. The situation is even more disappointing for the major commodity groups such as cereals, pulses and oilseeds and wool. These commodities comprise about 70 per cent of the State's gross value of agricultural production (GVAP) (Islam, 2000). Cereals (mainly wheat) comprises about 45 per cent of the GVAP but only four per cent are processed, including two per cent exports. On the other hand, the meat industry processes about 80 per cent (including 25 per cent for exports) of meat producing animals in WA. However, recent trends indicate that increasing proportions of beef cattle are now exported live (Islam and Johnson, 2003). As mentioned earlier, WA accounts for only four per cent of the national exports of meat products, while its share in national live animal exports is 40 per cent. TABLE 2.2 Percentage distribution of processed and unprocessed agricultural commodities produced in WA for domestic use and exports in a typical year

Notes: (a) Refers to cattle and sheep stocks and (b) Refers to the dairy industry, the unprocessed amount of milk refers to white market milk. Technically, all market milk also goes through some form of processing, bottling and packaging. Source: Islam (1997) Table 2.2 reveals that an insignificant proportion of agricultural commodities produced in Western Australia are processed and exported. Overall, although around 75 per cent of the primary production is exported, only 11 per cent is in processed form. This indicates that there are tremendous opportunities to benefit from the expansion of processing primary agricultural commodities in WA. In this paper we take the position that untapped opportunities exist in Western Australia for the further development of the State's agricultural processing sectors. Islam and Johnson (2003) identified impediments to expansions of agricultural processing in Western Australia . On the basis that these impediments can be reduced, through a combination of State Government policy and industry innovation, there exists within the State opportunities to process existing agricultural produce without the need for any expansion to local or world demand. 3. The WA ModelThe use of Computable General Equilibrium (CGE) models for economic analysis began in Australia with the creation of the ORANI model (Dixon et al. 1982). ORANI, in its original form, is a single-region model of the Australian economy; that is, it models the entire Australian economy, without any consideration of state level activities. Since the inception of ORANI, a variety of CGE models have been developed in Australia , including models which capture state level activities. One such model is WAM (the WA model) (Clements et al . 1996) which is used for the analysis in this report. 3.1 Characteristics of CGE ModelsCGE models have many advantages over other methods of economic analysis, such as input-output analysis. Whereas input-output analysis assumes the economy remains static (i.e. that price levels, labour to capital ratios and import shares remain unchanged throughout the analysis), CGE models are able to incorporate and predict changes to the economic structure. CGE models are able to do this because they contain equations describing a wide range of economic activities, including production, consumption, investment, employment, taxation and trade. CGE models consist of two major components: the equations and the database. While the equations give the model its predictive power, they are of no use without a comprehensive data set. The data incorporated into the model specifies the structure of the economy being analysed, and tells the model how variables react to changes in other variables. The economic structure is specified in CGE models with the inclusion of an input-output table. Input-output tables describe the transactions occurring within the economy in great detail, including, the transactions occurring between industries and the transactions occurring between industries and final consumers. How variables react to each other is specified by the elasticities of the database. 3.2 The WA ModelThe WA model (WAM), used for the analysis in this report, is similar in many respects to ORANI. Just like ORANI, WAM is formulated in percentage change terms. WAM also treats Western Australia as a single region, and contains an extensive set of equations describing production, consumption, investment, employment, taxation and trade within the State's economy. Therefore, it can be said that WAM is structured in a fairly standard way for CGE models in Australia . What distinguishes WAM, and makes it such a useful tool for economic analysis in Western Australia , is the model's database. The WAM database contains the most detailed information available on the economy of Western Australia . The input-output table currently used in WAM is a 108-sector table for the financial year 1994/95. The table is based on the 105-sector table for WA developed by Johnson (2001), with additional detail provided in primary agricultural industries (see Appendix 1). The original version of WAM (Clements et al. 1996) contained less detail than the current version, as its database was based on the 42-sector input-output table for 1989/90 (Clements and Ye, 1995). Even though it was less disaggregated than the current version of the model, it was still a highly effective tool for economic analysis, and was used to analyse such issues as:

WAM also became the basis for a variety of more specialised models: models such as WAT - a two-regional model of the WA economy - which was used to determine the impact of the Hot Briquetted Iron plant on the economy of the Pilbara region (Johnson, 1999), and WAE - a CGE model that incorporates energy substitution - which was used to investigate the impact of greenhouse gas reduction policies on the WA economy (Ahammad et al. 2001). 3.3 Modifications to WAMIn WAM, there are only two primary factors of production, labour and capital - where capital, in agricultural sectors, is a composite of land and capital. It is assumed in WAM simulations that labour is mobile across industries, and that the total supply of labour is not limited. Therefore, all industries can demand as much or as little labour as they require. Capital, on the other hand, is assumed to be industry specific and fixed in supply. Now, for certain primary agricultural industries this treatment of capital is unnecessarily, and unrealistically restrictive. In the application of WAM in this paper, we assume that some agricultural industries can 'share/swap' capital. The industries covered by this assumption are separated into two groups:

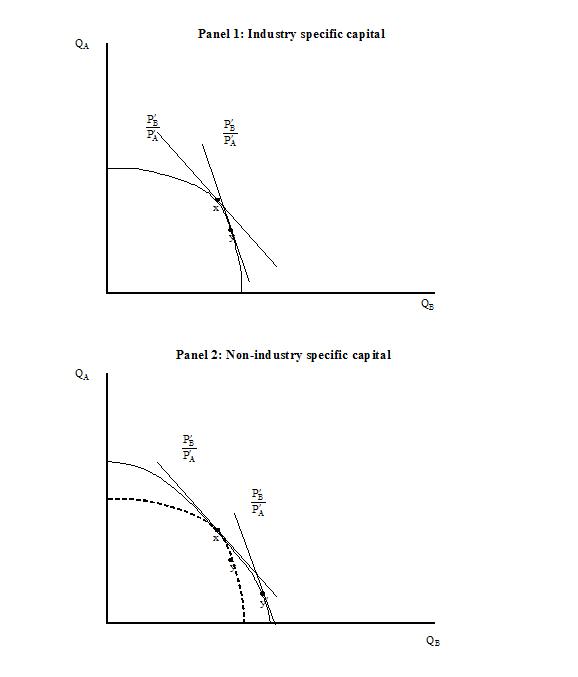

The numbers after each industry represent their position within WAM's industry structure. For the industries within each group, the capital stocks are allowed to vary; however, the capital stock for the group as a whole is assumed to be fixed, so that the following equations hold: (3.1) KA = K1 + K2 + K3 +K4 , and (3.2) KB = K8 + K9 + K10, where Ki (i = 1-4, 8-10) represents the capital stock in each industry, and KA and KB are both fixed. As part of WAM's determination of economic variables, the change in the price paid to units of capital is calculated. This price, PiK (where i = 1-4 for Group A industries, and i = 8-10 for Group B industries), provides the signal for capital redistribution within each group. For example, if the price paid to capital in the Sheep meat industry ( P1K) exceeds the price paid to Cereals ( P3K ), then capital will shift from the Cereals industry to the Sheep meat industry until the prices are equal. In other words, capital stocks redistribute between industries in Group A until (3.3) P1K = P2K = P3K = P4K. Similarly, for Group B industries capital redistribution occurs until (3.4) P8K = P9K = P10K. Equations (3.1) to (3.4) are in levels, while, as stated previously, WAM is formulated in percentage changes. The percentage change versions of these equations are not presented here; however, they are contained in Appendix 2. Appendix 2 also contains an alternative approach for deriving the percentage change versions of equations (3.3) and (3.4). 3.4 Impact of the modificationsWith the modifications described above, there is, potentially, a significant effect on model outcomes for those industries in Groups A and B. To describe the nature of these effects, we present a simple graphical analysis using production possibility frontiers. To do this, we assume the existence of an economy which produces only two goods, A and B. Panel 1 of Figure 3.1, presents the production possibility frontier for these two goods. The quantity of good A produced ( QA) is shown on the vertical axis, while the quantity of good B produced ( QB) is shown on the horizontal axis. The curve shown in panel 1 is the production possibility frontier for the production of these two goods, under the assumption that the capital employed in this two-good economy is industry specific, and cannot be shifted from the production of A to the production of B, and vice versa. In this simple system, the point at which production occurs is the point where the slope of the production possibility frontier is equal to the slope of the price line; where the slope is given by the price of good B ( PB ) relative to the price of good A ( PA ). Initially, with the relative price at PB/PA, the economy produces at point x on the production possibility frontier - which we assume to be a position of long-run stability, where capital in each industry is employed at maximum efficiency. Next, due to some disturbance in the economy, prices shift to P'A and P'B (relative price P'A/P'B ), and a new equilibrium is established at the point y, where the production of good A has diminished, and the production of good B has increased.

Figure 3.1 Production possibilities under different capital assumptions. Now, consider panel 2 of Figure 3.1. Here, it is assumed that capital is not industry specific, but may be shifted between industries. The original production possibility frontier is shown as the dotted curve in panel 2, with the new frontier shown as the solid curve. Note that the new curve touches the old at only one point: x. Recall that it was stated above, that point x represented a position of long-run stability, where capital in each industry is employed at maximum efficiency; therefore, no additional production of A or B is available at point x by redistributing capital. The remainder of the new production possibility frontier is outside the old frontier, and is the envelope of all possible capital-constrained production possibilities. Given the same economic disturbance, and the same shift in prices, that we saw in panel 1, a new equilibrium is established at point y1 in Panel 2. As is clear, the movement from point x to point y1 represents a more dramatic shift in the production pattern than does the movement from x to y, i.e. there is a greater reduction in the production of good A, and a greater increase in the production of good B. These larger changes occur because of the ability of capital to shift between the two industries. This analysis suggests that within WAM, under the assumption of joint capital, it can be expected that more pronounced changes in production will occur within Group A and Group B industries than could otherwise be expected. The magnitude of these effects will be studied in Section 4. 3.5 The simulationsThe industry structure used in WAM includes ten primary agricultural industries. Also within WAM's industry structure are numerous industries that process the output of these primary agricultural sectors. These include:

As discussed in Section 2, in this paper we take the position that opportunities exist for expansion of agricultural processing in Western Australia, and that these opportunities could be exploited without the need for any further increase in local or world demand (although changes to State Government policy and local industry innovation may be required). In Section 4, we use WAM to estimate the impact on the economy of Western Australia of an expansion in the above eight processing sectors. In other words, we investigate the impact of positive supply side shocks to these industries. So as to provide easily comparable results, the simulations are performed on the basis of a $1 million expansion in the output of each of these industries. In order to conduct these simulations, the $1 million expansions were first converted into percentage changes in the output of these industries. These changes then provide the inputs or 'shocks' to the model. The calculation of these shocks is presented in Appendix 3. 4. SIMULATION RESULTSIn this section, we present the results of the simulations designed to predict the impact on the WA economy of a $1 million expansion in each of eight agricultural processing industries. [5] The simulations were performed using the WA model (WAM) described in the previous section. We begin by looking at the impact of the expansion on key macroeconomic variables, before considering industry level impacts. 4.1 Macroeconomic impactsConsider the results presented in Table 4.1. For the $1 million increase in the output of the eight agricultural processing industries shown in column 1, the resulting increases in real Gross State Product (GSP), the consumer price index (CPI), employment, imports and exports, are provided in columns 2 to 6 of the table. Clearly, the table shows that the agricultural processing industry with the most beneficial impact on the State's GSP is the Wine and spirits industry, with GSP estimated to grow by $1,035,000 for every $1 million increase in its output. Beer and malt is the next most expansionary agricultural sector, followed by Fruit and vegetable products. Textile fibres, yarns and woven fabrics, with a GSP impact of $381,000, has the lowest impact. To understand the ranking of real GSP impacts revealed in Table 4.1, consider Table 4.2, which shows the input coefficients for the eight agricultural processing industries. Row 26 of Table 4.2 shows the direct contribution to GSP of a $1 expansion in the output of each industry. Beer and malt, Fruit and vegetable products and Wine and spirits have, in that order, the highest direct GSP contributions of the eight industries shown. Textile fibres, yarns and woven fabrics has the lowest direct contribution. The ordering of direct GSP contribution is therefore very similar to the ordering of impacts shown in Table 4.1. This not surprising as the results in Table 4.1 show the direct plus indirect effects, or total effects. However, the direct GSP contribution alone does not account for the ranking of real GSP impact shown in Table 4.1, however they are critical. The direct effects are important for two main reasons. The first, and obvious one, is that they show the direct impact of the expansion on real GSP. The second reason is that private consumption in WAM is a linear function of real GSP. The direct stimulus from the expansion in agricultural processing flows immediately on to consumer spending. Why then is the direct GSP effect not a perfect predictor of the real GSP effects shown in Table 4.1? The reason is the flow-on effects captured by the WAM simulations. Row 20 of Table 4.2 shows, for each agricultural processing industry, the share of inputs to production sourced from within Western Australia . Consider the industries Beer and malt, Fruit and vegetable products and Wine and spirits (columns 7, 4 and 8 respectively). Wine and spirits has the highest local input use of these three industries, indicating that the flow-on effects generated from its expansion are likely to be higher than the flow-on effects generated by the other two industries (although this should be viewed as a 'rule-of-thumb' rather than a rigorous relationship). This is why Wine and spirits ranked the highest in real GSP impact, even though it ranks only third in direct GSP impact. Table 4.1 shows that the CPI and employment impacts of agricultural expansion follow a similar pattern to the total GSP impact, with the $1 million expansion in Wine and spirits creating the most jobs, 22, and increasing the CPI by 0.0015 per cent - this CPI increase is rather insignificant, but remember we are dealing with a relatively small increase in output. The expansion in the Textile fibres, yarns and woven fabrics industry increases employment by only 11 persons, and increases the CPI by 0.0005 per cent. The CPI effects follow precisely the same ranking as the impacts on real GSP. This is to be expected. As described above, private consumption in WAM is a linear function of real GSP; therefore, it is to be expected that the industries generating the highest GSP effects will increase private consumption by the most, and hence produce the highest increase in consumer prices. Table 4.1. Macroeconomic impact of an expansion in agricultural processing industries

Consider the impact on imports, shown in column 5 of Table 4.1. The expansion of the Textile fibres, yarns and woven fabrics industry produces the smallest increase in imports. The Oils and fats industry produces the largest increase. This is not a surprising result, as the Textile fibres, yarns and woven fabrics industry has one of the lowest import propensities among the agricultural processing industries (just over three per cent), while oils and fats has the highest (22 per cent), as can be seen from row 24 of Table 4.2. Next, column 6 of Table 4.1 shows the increase in exports resulting from the expansion in agricultural processing. The smallest increase in exports occurs with the expansion of the Textile fibres, yarns and woven fabrics industry, and the largest occurs with the Oils and fats industry. This is the same result as we found for imports, which is to be expected. Industries that consume few imports will consume more locally produced commodities when they expand. Much of this increased domestic consumption will be at the expense of exports. So, while most of the expanding industries output may be exported, there will be a high level of absorption by that industry of local commodities that would otherwise have been exported. Likewise, high importing industries have lower domestic absorption, and consequently their expansion results in higher exports. 4.2 Industry impactsIn addition to its ability to estimate impacts at an economy wide level - the macroeconomic effects - WAM is able to estimate impacts for each of the 108 industries in the model. Here, we consider these industry level impacts. However, before examining the results of the WAM simulations, it is useful to discuss the industry-industry interactions in the model's input-output database, as the relationships revealed will help us to interpret the modelling results. Table 4.2 Input coefficients for agricultural processing industries (percentages)

Table 4.2 contains a summary of the key industry relationships from the input-output table used in the WAM database. The columns of the table present the consumption shares (in percentages) for intermediate inputs and primary factors in agricultural processing industries. For example, column 2 summarises the purchases made by the Meat and meat products industry when producing its output. To save space, consumption from all of the 108 industries in the database is not provided. What is provided is a full list of the input shares of the primary agricultural industries (rows 1 to 10 of Table 4.2), a full list of input shares from the eight agricultural processing industries (rows 11 to 18), the total share of inputs of other - non-agricultural - goods and services (row 19), the share of total intermediate inputs in production (row 20), and finally (in rows 21 to 24), the share of inputs/costs covered by Compensation of employees (wages), Gross operating surplus (profits), Taxes and Imports. As the figures in each column represent cost/input shares in percentage terms, they sum to one hundred, as shown in row 25. From the information in Table 4.2 we can see which industries - particularly which primary agricultural industries - are most closely associated to the eight agricultural processing industries. Starting with the Meat and meat products industry (column 2 of Table 4.2), we see that the industry takes inputs from the Sheep meat (12 per cent), Beef cattle (28 per cent), Pigs (5 per cent) and Poultry (9 per cent) sectors, all of which will benefit from any expansion in the output of Meat and meat products. The expansion of the Dairy products industry (column 3) will be of most benefit to the Dairy cattle industry, as Dairy cattle supplies 34 per cent of its inputs. An expansion in the Fruit and vegetable products industry (column 4) will benefit Horticulture (with 3 per cent of inputs) and New industries (5 per cent) the most. The Pulses and oilseeds industry (with 4 per cent of total inputs) is the most significantly linked primary agriculture sector to the Oils and fats industry (column 5). In spite of this, it is interesting to note that Oils and fats gains an even higher share of its inputs from the Meat and meat products industry (5 per cent), with an even larger share still supplied from within the industry itself (10 per cent). Flour mill products and cereal foods (column 6) derives 18 per cent of total inputs from Cereals, while the Beer and malt industry (column 7) derives 10 per cent of its inputs from Cereals. The Wine and spirits industry (column 8) takes significant inputs from Horticulture (5 per cent) and New industries (11 per cent). Finally, the Textile fibres, yarns and woven fabrics industry (column 9) derives a massive 58 per cent of its total inputs from Wool, clearly the most significant relationship demonstrated in Table 4.2. Keeping the relationships between the agricultural processing and primary agriculture industries in mind will aid with the interpretation of the WAM simulation results presented in Table 4.3. The impact of the expansion of the agricultural processing industries on the primary agricultural sectors are shown in rows 1 to 10 of the table. Consider first the results for the expansion of the Meat and meat products industry (column 2). As expected, we see an expansion in the primary agricultural industries of Sheep meat, Beef cattle, Pigs and Poultry, although the expansion in the later three sectors is relatively small compared to the expansion in Sheep meat output of $134,000. Recall that the industry Sheep meat is part of a group of agricultural industries which share capital (the Group A industries described in the previous section). These industries are capable of shifting capital (which includes agricultural land) between the production of the different Group A commodities (Sheep meat, Wool, Cereals, and Pulses and oilseeds) even though the total stock of capital available has not changed. With the expansion of the Meat and meat products industry, the demand for Sheep meat, Beef Table 4.3. Industry impact of an expansion in agricultural processing industries ($'000)

cattle, Pigs and Poultry all increase. For the industries Beef cattle, Pigs and Poultry, most of the increased domestic demand for their output is met by reducing exports, with only a small increase in their total production. Sheep meat, which is able to gain access to more capital - at the expense of the Wool, Cereals and Pulses and oilseeds sectors - is able to meet more of the increased domestic demand by increasing production. With the ability of the Sheep meat industry to command more capital at the expense of the Group A industries, it is not surprising to see that the output of these other industries diminishes, with the output from the Cereals industry falling by $66,000. It is interesting to note that the output of the Wool industry falls by a far less significant $8,000. This indicates that farmers will not increase Sheep meat production by significantly shifting capital away from Wool, but, rather, by decreasing the capital (which we should remember includes land) available to Cereals, and to a lesser extent Pulses and oilseeds. Table 4.4 shows for the eight simulations the estimated changes in capital dedicated to the industries in Group A and Group B. The first thing to note about this table is that the elements all represent very small changes in capital stocks. However, it should be remembered that the expansion of WA's agricultural processing sectors by $1 million caused only a relatively minor disturbance to the primary agricultural sectors (compared to their overall size), and so minor adjustments are to be expected. The second thing to note is that within each group the adjustments to capital stocks sum to zero, demonstrating that within each group the capital stocks remain fixed. [6] Table 4.4. Adjustments to capital stock in agricultural industries (percentages)

Note: 1) The summation of industry effects (columns 3 to 10) are share weighted sums (see column 2 for capital shares). As expected, Table 4.4 shows that an expansion in the Meat and meat products industry causes capital in Group A to be redistributed to Sheep meat, and away from Wool, Cereals, and Pulses and oilseeds. At the same time, the expansion in the output of Meat and meat products has little impact on capital stocks in Group B. Returning our attention to the changes in industry output shown in Table 4.3, we find that the total impact of the expansion in Meat and meat products on primary agricultural industries, presented in row 11 of the table, is an expansion of $118,000. This increase is due largely to the expansion in output in the Sheep meat industry of $134,000. The output in some of the sectors within primary agriculture - Wool, Cereals and Pulses and oilseeds - actually falls due to the expansion in output of the meat and meat products industry. This mainly occurs as a result of the sheep meat sector demanding more capital at the expense of other industries in Group A (see Section 3 for more detail on these effects). It should be noted that the total change in primary agriculture, while positive for meat and meat products expansion, is not positive for all processing developments shown in columns 3 to 9. The reason behind the negative values will be discussed later in this section. Next, consider the impact of the expansion of the Meat and meat products industry on industries outside of primary agriculture. Rows 12 to 19 of Table 4.3 show the impact on the agricultural processing industries. Amongst the agricultural processing industries there are only minor changes, with the exception, of course, of Meat and meat products, where a million dollar expansion is shown. Overall, the expansion in agricultural processing industries is just less than the $1 million dollar expansion experienced by Meat and meat products. Despite the fact that several agricultural processing industries are themselves suppliers (although of relatively small quantities) to the meat and meat products industry, the impact on these sectors of the expansion in meat and meat products output is zero or slightly negative. To understand why this occurs, it is important to remember that, like the primary agricultural industries, the agricultural processing industries are themselves exporters of their products. With an expansion of the domestic economy, and the subsequent - although small - rise in the general level of prices, the local currency experiences a real appreciation against foreign currencies (whose price levels remain unaffected by the local economy). The effect of such an appreciation is to reduce local exports. [7] It is clear that for industries such as Dairy products, the negative impact of the real appreciation outweighs the increase in demand from local industry. Growth in non-agricultural based industries is given in row 21 of Table 4.3. These sectors experience growth of $749,000 as a result of the expansion in the Meat and meat products industry. When this is added to the output growth expected in the primary agricultural and agricultural processing industries, the total growth in output in the Western Australian economy is $1.85 million (row 22). A similar examination of the impacts of the other seven agricultural processing industries could be performed; however, it would be rather time consuming, and so only some of the key features will be discussed. Most interestingly, we see that for many of the expanding industries the change in the output of total primary agriculture (row 11) is in fact negative. This can occur for two reasons. The first is the real appreciation of the local currency, which we discussed earlier in relation to agricultural processing industries. The same principles apply to primary agricultural industries that are exporting. That is, the real appreciation of the local currency makes exports of primary agricultural products less competitive relative to international primary agricultural products, and so exports fall. The other reason for the fall in output is to do with the capital adjustments occurring to industries in Groups A and B. Within these groups, capital is shifted so as to equate payments to capital, which in turn maximises the overall returns to capital. Maximisation of returns does not necessarily mean maximisation of output, and so it is possible that a farm that adjusts its usage of capital to maximise its returns, may in fact reduce its output. To this point we have considered the industry impacts of expansion in agricultural processing industries at a very detailed level. To complete this section we take a step back, and consider the broad sectoral effects of the expansion in agricultural processing, which are shown in Table 4.5. Here we note that it is the Manufacturing sector that increases its output by the largest amount; but this, of course, is to be expected, as the agricultural processing industries are themselves part of manufacturing. The other sectors doing particularly well from the expansions in agricultural processing are trade and transportation and services. 5. SUMMARY AND CONCLUSIONThis study investigated the economy-wide benefits available to Western Australia through further processing of the state's primary agricultural products. This investigation was undertaken utilising a Computable General Equilibrium (CGE) economic model of Western Australia . This model - known as WAM - is a multi-sectoral model of the WA economy with a specific focus on the state's agricultural sectors. Table 4.5. Change to broad sectoral outputs ($'000)

In Section 2, the nature and extent of WA's agricultural processing sector was described, and contrasted with the level of processing occurring in the other states of Australia . Section 3 discussed the characteristics of CGE models in general and the WA model (WAM) in particular. The theoretical structure underpinning WAM was also described in this section. WAM was used to simulate the effects of a $1 million expansion in eight agricultural processing industries, and in Section 4, the results of these simulations were presented and discussed in detail. 5.1 Major findings of the studyThe broad impacts of growth in agricultural processing are summarised in Table 5.1. The table shows that there is a range of potential impacts from agricultural processing. Clearly, the most significant impact is derived from the expansion of the Wine and spirits industry. Table 5.1 demonstrates that such an expansion is estimated to increase the State's GSP (Gross State Product) by $1,035,000, and to increase total output by $2.2 million. The expansion of the Wine and spirits industry is also estimated to have the largest impact on employment, with 22 new jobs created. Table 5.1 also shows that expansion of the Textile fibres, yarns and woven fabrics industry has the least beneficial effect on the economy, with GSP rising by just $381,000, and only 11 new jobs created. Table 5.1. Impact of an expansion in agricultural processing industries

5.2 ConclusionsAlthough food and agricultural processing in WA started from the beginning of European settlement in 1829, the industry as a whole remains in its infancy. In the last decade or so, globalisation of the industry offered the potential to attract a new generation of investment opportunities focused on supplying the Asia-Pacific region, but it appears that the food processing industry in Australia as a whole, has squandered this opportunity (IPA, 2001). Global forces provide both opportunities and threats but the failure of industry to take advantage of those opportunities only increases potential threats. Since this study indicates that the Western Australian economy gains from the expansion of the agricultural processing industries, and private investment is insignificant, the government sector has an important role to play in helping the industry to capture those benefits. If essential logistic and institutional supports are made available, the agricultural processing industries in WA can still expand even with its small local market and less competitive supply of raw materials. It is, therefore, important for the public sector to develop and implement appropriate policies to remove barriers to private investment in agricultural processing in Western Australia . REFERENCESAFFA (2002). National Food Industry Strategy: An Action Agenda for the Australian Food Industry. Canberra : Department of Agriculture, Forestry, and Fishery - Australia , Commonwealth of Australia . Ahammad, H. and Clements, K.W. (1999). 'What Does Minerals Growth Mean to Western Australia ?' Resources Policy 25: 1-14. Ahammad, H., Clements, K.W. and Ye, Q. (2001). 'The Regional Economic Impact of Reducing Greenhouse Gas Emissions: Western Australia .' Resources Policy, 27: 255-233. Ahammad, H. and Greig, R. (2000). 'A Regional Perspective on Tariffs: The Western Australian Experience.' Australasian Journal of Regional Studies 6: 67-94. Australian Bureau of Statistics (2001). Australian National Accounts: State Accounts. Canberra : AGPS. ABS Catalogue No. 5220.0. ________ (2001a). Manufacturing Industry Australia . Canberra : AGPS. ABS Catalogue No. 8221.0. ________ (2001b). Manufacturing Industry Western Australia . Canberra : AGSP. ABS Catalogue No. 82215.0. ________ (2002). Consumer Price Index. Canberra : AGSP. ABS Catalogue No. 6401.0. Clements, K.W., Ahammad, H. and Ye, Q. (1996). 'The Economics of New Mining and Mineral-Processing Projects in WA: Effects on Employment and the Macro Economy.' Resources Policy 22(4): 293-346. Clements, K.W. and Johnson, P.L. (2000). 'The Minerals Industry and Employment in Western Australia : Assessing its Impacts in Federal Electorates.' Resources Policy 26: 77-89. Clements, K.W. and Ye, Q. (1995). A New Input-Output Table for Western Australia . Nedlands: Economic Research Centre, The University of Western Australia . Clements, K.W., Ye, Q. and Greig, R.A. (2002). The Great Energy Debate. University of Western Australia Press, Perth . DFAT (1998). Composition of Trade Australia 1998. Department of Foreign Affairs and Trade, Canberra . Dixon , P.B., Parmenter, B.R., Sutton, J. and Vincent, D.P. (1982). ORANI: A Multisectoral Model of the Australian Economy. Amsterdam /New York/Oxford: North-Holland Publishing Company. Gregory, R.G. (1976). 'Some Implications of the Growth of the Minerals Sector.' Australian Journal of Agricultural Economics 20: 71-91. International Trade Centre, (1998) UNCTAD/WTO. IPA (2001). Take Away Take-Away: The Self-Induced Destruction of the Australian Food Manufacturing Industry, (The second publication of the IPA's Work Reform Unit, November 2001) http://www.ipa.org.au/pubs/workreform/foodfs.html. Islam, N. (1997) Agriculture and the Western Australian Economy: Value Added Contribution of Agricultural commodities, Office of Policy and Planning, Agriculture Western Australia , South Perth , December. ________ (2000), 'An Analysis of Productivity Growth in Western Australian Agriculture', Discussion Paper 00.15, Department of Economics, UWA, Nedlands. Islam, N. and Johnson, P. (1997). Agriculture and the Western Australian Economy: An Input-Output Analysis - Volumes 1 and 2. South Perth : Agriculture Western Australia . ________ (2003). Agricultural Processing and the Western Australian Economy. South Perth : Agriculture Western Australia . Johnson, P.L. (1999). 'The Impact of Major Projects on Regional Economies: The Case of HBI in the Pilbara.' Papers and Proceedings PhD Conference in Economics and Business. Perth : The University of Western Australia and The Australian National University . Johnson, P.L. (2001). An Input-Output Table for the Kimberley Region of Western Australia . Kimberley Development Commission. APPENDIX 1.INPUT-OUTPUT TABLE FOR USE IN WAMThe database of the original WA model (WAM) was based on the input-output table for Western Australia for 1989/90 developed by Clements and Ye (1995). For the application of WAM in this report, it was desirable to have the database based on a more recent Western Australian input-output table. The most recently published State table is for 1994/95 (Johnson, 2001). However, before this table was incorporated into the WAM database it was enhanced to provide more detail for primary agricultural industries. In the original 1994/95 table, there were seven primary agricultural industries. Three of these industries, Sheep, Grains, and Other agriculture, were disaggregated into Sheep meat and Wool; Cereals, Pulses and oilseeds; and Horticulture and New industries. This disaggregation was achieved by utilising a previous input-output table for Western Australia developed by Islam and Johnson (1997). Islam and Johnson's table was developed for the year 1992/93, and the primary agricultural sectors in that table had already been disaggregated in the manner specified above. Therefore, the primary agricultural sectors of Sheep, Grains and Other agriculture in the 1994/95 table were split, based on the proportions demonstrated in the 1992/93 table. With this split, the new table for 1994/95 contained 10 primary agricultural sectors:

With the disaggregated table determined, the structure of the agricultural sectors was reviewed, with particular emphasis on the newly disaggregated industries. Only one anomaly was discovered, the Gross operating surplus (GOS) - which represents profits accruing to the owners of capital - of the Wool industry represented only 16 per cent of total costs for that industry, whereas the GOS of the Sheep meat industry was 46 per cent of its total costs. Such a large disparity is difficult to understand and was traced back to an error in the 1992/93 table of Islam and Johnson (1997). The anomaly was removed by assuming that the GOS of the Wool industry corresponded to the national share for the Sheep industry - 44 per cent. APPENDIX 2.ADDITIONAL WAM EQUATIONSThe full set of equations for the WA model (WAM) will not be presented here, but are available in Clements et al . (1996). In this appendix, we consider only those equations added to WAM to incorporate jointness in primary agricultural production. As was described in Section 3 of this report, selected primary agricultural sectors are able to swap capital. In the basic WAM structure this is not possible, as capital (really a composite of land and capital) is industry specific and cannot be used by another industry. To incorporate this aspect of 'jointness' in agricultural production, two groups of industries are assumed to be capable of sharing capital: Group A: Sheep meat (1), Wool (2), Cereals (3) and Pulses and oilseeds (4) Group B: Horticulture (8), New industries (9) and Dairy cattle (10), where the numbers after each industry represent the industry's position within the WAM industry structure. Letting K represent the capital stock in each industry, it follows that: (A.1) KA = K1 + K2 + K3 +K4, and (A.2) KB = K8 + K9 + K10, where KA and KB are both fixed. As WAM is formulated in percentage change terms, the above equations need to be rewritten in percentage change form before they can be incorporated into the model. By convention, the percentage change form of WAM variables are written as lower case letters. Equation (A.1) therefore becomes (A.3) and (A.2) becomes (A.4) In equation (A.3), kj is the percentage change in the capital stock of all Group A industries, kj (j = 1-4) is the percentage change in the capital stock of individual Group A industries, and The process of determining the equilibrium distribution of capital between Group A and between Group B industries relies upon the price paid to each unit of capital ( PiK). It is assumed that at equilibrium the price paid to capital in each industry is the same, i.e. for Group A industries. (A.5) P1K = P2K = P3K = P4K. Similarly, for Group B industries (A.6) P8K = P9K = P10K. Converting equations (A.5) and (A.6) into percentage changes, we have for Group A industries (A.7) p 1K = p2K = p3K = p4K, and for Group B industries (A.8) p8K = p9K = p10K. An alternative approach to determining the equilibrium price relationship is to calculate the rate of return on capital in each industry. Following Dixon et al. (1982), the net rate of return to fixed capital ( Rj ) is given by (A.9) where PjK is the user's price of capital to industry j, (A.10) where Qj = ( Rj + dj ) / Rj is the ratio of the gross rate of return to capital to the net rate of return. In the short-run, where capital stocks are fixed, so is the cost of capital to industry j (where the cost represents the price paid in the production of the existing units of capital). Therefore, the change in the cost of these existing units of capital, If it is assumed that Rj and dj are the same for each industry in Group A, and for each industry in Group B, then it follows that at equilibrium the return to capital in each group will equalise, and, therefore, the price paid to capital in each industry will also equalise. Thus, in the short-run equilibrium for Group A industries is represented by (A.11) p 1K = p2K = p3K = p4K, while for Group B industries, (A.12) p8K = p9K = p10K. These are equivalent to the results obtained earlier. APPENDIX 3.CALCULATING THE SHOCKS USED IN THE WAM SIMULATIONS

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Ind |

Processing industry |

Total production |

Output shock |

(1) |

(2) |

(3) |

(4) |

20 |

Meat and meat products |

932.5 |

0.0901 |

21 |

Dairy products |

309.9 |

0.2711 |

22 |

Fruit and vegetable products |

165.8 |

0.5066 |

23 |

Oils and fats |

44.1 |

1.9048 |

24 |

Flour mill products and cereal foods |

100.8 |

0.8333 |

29 |

Beer and malt |

288.3 |

0.2914 |

30 |

Wine and spirits |

76.8 |

1.0938 |

31 |

Textile fibres, yarns, fabrics etc. |

140.7 |

0.5970 |

Notes:

1. Total production values are taken from the WAM database.

The simulation results presented in Section 4 of this report relate to a $1 million increase in the output of the agricultural processing industries. In this appendix, we present a different approach to the expansion of the agricultural processing industries. Here, we consider a 10 per cent increase in the value of output of each of these industries. (Where the 10 per cent change is relative to the size of the industry in 1994/95, the base year of the database.)

Table A4.1 presents the results of the simulations conducted to determine the economic impact of a 10 per cent expansion in the output of agricultural processing industries. Clearly, the most economic benefit is derived from the expansion of the Meat and meat products industry, with real GSP expanding by 0.12 per cent. This is substantially more than the meager 0.007 per cent increase in real GSP associated with a 10 per cent expansion of the Oils and fats industry. However, in interpreting these results it must be remembered that the Meat and meat products industry - with output valued at $930m in 1994/95 (see column 3 of Table A3.1) - is more than 20 times larger than the Oils and fats industry - which had output valued at only $44m in 1994/95. As such, the results in Table A4.1 are to interpreted cautiously, as much of the difference between industry impacts is due to the relative sizes of the expanding industries.

However, relative industry sizes are clearly not the only factors of importance. Consider the results for the Dairy products and Fruit and vegetable products industries in Table A4.1. Even though the Dairy products industry is nearly twice the size of the Fruit and vegetable products industry (see column 3 of Table A3.1), the economic impacts from a 10 per cent increase in the output of each are quite similar, with the real GSP of each rising by 0.031 per cent. As was shown in Table 3.1 in Section 4 - where a $1 million increase in output was considered - expansion in the Dairy products industry has considerably less flow on benefits to the WA economy than does expansion in the Fruit and vegetable products sector. This is reflected in the results presented in Table A4.1.

Table A4.1. Macroeconomic impact of a 10 per cent expansion in agricultural processing industries (percentage change)

Agricultural processing industries |

Real GSP |

CPI |

Employment |

Imports |

Exports |

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

Meat and meat products |

0.120 |

0.104 |

0.187 |

0.057 |

0.125 |

Dairy products |

0.031 |

0.029 |

0.050 |

0.018 |

0.033 |

Fruit and vegetable products |

0.031 |

0.026 |

0.048 |

0.023 |

0.035 |

Oils and fats |

0.007 |

0.006 |

0.011 |

0.008 |

0.010 |

Flour mill products and cereal foods |

0.016 |

0.014 |

0.026 |

0.009 |

0.016 |

Beer and malt |

0.058 |

0.050 |

0.084 |

0.035 |

0.060 |

Wine and spirits |

0.020 |

0.016 |

0.025 |

0.009 |

0.010 |

Textile fibres, yarns, fabrics etc. |

0.013 |

0.009 |

0.022 |

0.004 |

0.008 |

[1] Contributed paper presented to the 47th Annual Conference of the Australian Agricultural and Resource Economics Society, held at The Esplanade Hotel Fremantle, Western Australia, 11 - 14 February, 2003. This paper is an extract from the authors' longer research paper: Agricultural Processing and the Western Australian Economy, Department of Agriculture Western Australia , South Perth , January 2003.The authors wish to acknowledge Ian Longson and Graeme Wilson for their support in completing the study. Sincere gratitude and thanks are also owed to Professor Ken Clements for the intellectual and logistical support he provided throughout the study. The views expressed in this paper are not necessarily the views of the Department of Agriculture Western Australia .

[2] Department of Agriculture Western Australia (AGWEST) web page, http://www.agric.wa.gov.au/programs/trade/ html/12compb.htm.

[3] During 1994 to 1998, Australia 's processed food exports grew by just 1.8 per cent compared with 21 per cent for the USA , 10 per cent for Germany and 9 per cent for France (International Trade Centre, 1998). As a result, Australia 's global market share decreased from 3 per cent to 2.8 per cent. However, Australia 's exports of unprocessed food grew by 40 per cent during the period (DFAT, 1998).

[4] Although food processing is only a subset of all agricultural processing, it is used in this section to demonstrate the differences between Western Australia and the other Australian States and Territories .

In Appendix 4 an alternative set of results are presented. These demonstrate the impact arising from a 10 per cent increase in the output of the agricultural processing sectors.

[6] Where the summation is carried out on a share-weighted basis.

[7] The negative impact that expanding export industries have on other exporters is known in Australia as the Gregory Thesis (Gregory, 1976) and as the Dutch Disease in Europe and elsewhere (the Economist, 26 November, 1977, pp.82-83).

|

Contact the University : Disclaimer & Copyright : Privacy : Accessibility |

|

Date Created: 02 June 2005 |

The University of Melbourne ABN: 84 002 705 224 |