Australian

Agri-Food 2000 Research Forum

Melbourne August 17

The Applicability and Use of the Balanced Scorecard for the Farm Manager.

K.M. Rawlings 1, W.J. Parker 2 and N.M. Shadbolt 3

1 Institute of

Land and Food Resources, The University of Melbourne.

2 General Manager Science, Ag Research, Hamilton, New Zealand.

3 Institute of Food, Nutrition and Human Health, Massey University, New Zealand.

| Introduction |

| What is the Balanced Scorecard? |

| The Balanced Scorecard and Farming |

| Theory versus Practice |

| Discussion & Conclusion |

| Click

here for the PowerPoint Presentation |

Strategic management is not widely practiced in a formal manner amongst the farming community yet it is an important aid to achieving farm family and business goals. The family farm is a complex business due to the intimate interaction between business and lifestyle goals. Often these goals conflict and the farming family must reach some sort of compromise in order to meet their aspirations. This is not an easy task: it creates a dilemma for the farm’s owner, family and advisor, as each may have different needs and measure the realisation of these in different ways. Traditional measures of farm success are financial and production based; personal and family goals are rarely contemplated with respect to their measurement, as the farm’s strategy (if there is one) is implemented.

The perceived complexity of strategic planning and control is overwhelming to many farmers. Our aim was to explore whether the Balanced Scorecard approach to strategic management would improve farmers’ understanding, and simplify the processes involved in developing, implementing and monitoring farm strategy.

What is the Balanced Scorecard?

The Balanced Scorecard, developed by Robert Kaplan and David Norton in the early 1990s, is a strategic management tool that provides the manager with a clear and concise picture of the business’s health and progress in reaching the goals of the business. It was originally developed to improve the alignment of measures with strategy and thereby to assist in monitoring the success or otherwise of implementing strategy. Kaplan and Norton liken the Balanced Scorecard to that of an aeroplane’s cockpit controls. The scorecard addresses the basic aim of financial profit, the cornerstone of every business, by revealing the drivers to creating long-term financial and competitive performance through investment in areas such as employees, customers, partners and technology, amongst others (McCann, 2000). It also aims to close the gap between the business’ strategic vision and its day-to-day operations and decision making (Towle, 2000). The Balanced Scorecard achieves this by linking both financial and non-financial performance measures to the business’ vision and strategy.

A Balanced Scorecard is a set of financial and non-financial performance measures that reflect the factors that are considered to be critical to the success of the business. It gives managers important information from four different perspectives, which together offer a holistic view of the business's health. It also allows managers to consider all of the important strategic measures at the same time, letting them see whether improvement in one area is achieved at the expense of another (Kaplan and Norton, 1992; Butler et al, 1997).

The four perspectives as identified by Kaplan and Norton are:

The financial perspective that looks at how the business’ strategy is affecting the bottom-line. Therefore traditional measures such as growth, profitability and shareholder value are monitored. It would be unusual not to find a number of goals in this area of the Balanced Scorecard.

The customer perspective that asks the question "How do existing and new customers view and value us?" The answer to this question requires customer involvement, as they need to identify their expectations of the firm and how they measure the firm’s ability to achieve their goals. Newing (1995) emphasised that for most organisations the price factor only represents 30% of their customers’ total cost of acquiring materials or services. Therefore, businesses need to pay particular attention to identifying and understanding their customers’ requirements. Another question that should be considered is: "How are you affecting your customers’ results?"

The internal business perspective that focuses on the skills, competencies and technology of the business and its ability to meet the needs of the customer as well as the potential to add value to customers’ businesses.

The learning and growth perspective focuses on the business’ ability to change, improve and adapt their products and processes as well as the ability to develop and introduce new improved products and services (Kaplan and Norton 1992). The business must set targets that respond to continuous change in customer needs (Newing, 1995).

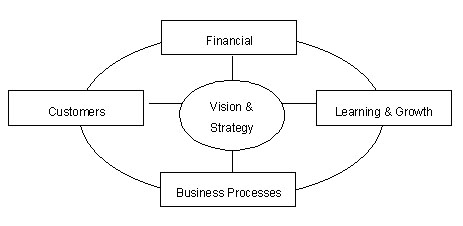

Figure 1 The Balanced Scorecard Framework. (Source: Kaplan and Norton 1996)

The Balanced Scorecard approach places the business’ vision and strategy firmly in the middle of the scorecard to ensure that focus is not lost. The business’ goals (strategic choices) each with its stated measures and drivers of success are then allocated to one of the four perspectives of the business.

The absence of goals or abundance of goals in any one perspective would give a quick, visual indication of whether the business is "in balance". The links, sometimes causal, between goals in different perspectives must then be examined to better understand the effect one might have on another. This understanding enables a short list of the key drivers of performance to be drawn up.

Identifying the relevant measures is a crucial step in a Balanced Scorecard development (Willyerd 1997). Once critical success factors are identified, measures must be established to monitor these.

The key concept of the Balanced Scorecard is the inclusion of non-financial indicators, which represent goal attainment and are key to the strategy. Financial indicators are generally lagging indicators that is they represent the past ie. what you have just accomplished. They have limited ability to predict future outcomes.

Focusing on these measures increases the focus on the present rather than what needs to be achieved in the future.

In contrast, non-financial indicators are usually leading, that is they inform the manager of likely future performance. For example, the learning of new knowledge and skills is a lead indicator of the farmer’s future focus and ability to manage. Without investment in staff learning and personal growth the business has less ability to cope with and manage change.

To design good measures it is necessary to understand what needs to be measured. Therefore, you must be clear about your criteria. Measures have to be meaningful to the situation and the people using them to allow informed decision making.

Measures that are aligned to strategic intent provide feedback for management control. They also communicate to all levels of the firm the business plan. A good scorecard tells the story of the business’ strategy, therefore creating a shared understanding.

The Balanced Scorecard and Farming

Farming in both New Zealand and Australia is primarily based on family businesses. While the literature on Balanced Scorecards is focused on the corporate sector, it does not preclude its application to the family farm. However to do this the elements of a family business, and how and why these differ from a corporate business, must be understood.

The family business mixes emotions and sentimentality with objectivity and rational calculation. The family and the business are inseparably linked despite the relative incompatibility of the two components. The family business, unlike a corporate, must deal with the demands of family relationships as well as the demands of the market place (Robbins & Wallace 1992).

Robbins and Wallace (1992) characterised the typical family business as having one or more of the following:

- An unclear business structure with no formal legal agreements.

- Poor definition of responsibility ie. who does what, where, when and with whom?

- Lack of formal hierarchy for responsibility and authority; especially important when non-family labour is employed.

- An owner/manager "tends to do everything while staff do nothing" syndrome ie. "No one can do it as well as I can".

- Failure and/or inability to plan business development.

- Inability to set specific business objectives, design and implement strategies and actions, and then periodically and systematically evaluate the situation.

- Poor succession planning.

In a farming context the four perspectives of the Balanced Scorecard can be approached as follows:

The internal business perspective is generally covered adequately in farm business plans. It covers the ability of the business to deliver and produce to specification, thus concentrating on the production processes (feeding, animal health, resources, staffing etc.) and efficiency of resource use. Production management has historically been the strongest focus of farm business management, both in practice and the literature (Parker, 2000b).

The customer and learning and growth perspectives, are generally poorly covered in most farming business plans. The importance of having goals for these area cannot be overemphasized.

These are areas in which a number of the non-financial goal dimensions ensure the production plans are aligned to current and future market needs, including environmental sustainability and livestock husbandry, an that the farm’s greatest assets, its people, are being developed and nurtured to deliver the innovation that is crucial to future business success.

Integrating plans for these perspectives into the farm strategy ensures a better balance of effort and greater emphasis on future family and market needs than focussing only on production and finance.

The Balanced Scorecard provides farm managers with a framework that allows them to visualise the interactions between the different components of their strategy. . This is demonstrated in Figure 2, which is based on an existing farm business plan. The Balanced Scorecard format helps the farm business to put its financial and non-financial goals into context and to identify conflicts between short and long-term viability.

The scorecard can help family businesses by aligning and focussing them on implementing long term strategy (Kaplan and Norton 1996a). The long-term vision that is a feature of strategic planning is less likely to be lost if the Balanced Scorecard is used in the strategic plan as it forces the farm business to link its goals to that vision.

The scorecard also forces farm businesses to ensure that they have goals that will deliver to each of the four perspectives thereby achieving a balance that has been found, in a large number of other businesses, to be vital to the business’ ability to deliver to its vision.

Theory versus Practice:Many articles can be found in the literature about the Balanced Scorecard and its application to strategic but there is as yet relatively little published empirical evidence. In conducting research to adapt the Balanced Scorecard to farming, 10 case studies were undertaken with owner-operator dairy farmers in the lower North Island of New Zealand (Rawlings, 1999). The aims were to identify goal conflicts and apply the Balanced Scorecards to the farmer’s future plans. However, a number of obstacles were encountered.

The first was the lack of formal value and goal identification. Values and goals are the foundation for strategic planning and indeed the Balanced Scorecard, thus they are integral to the process (Kaplan and Norton, 1992). However, their identification for some farmers was a difficult task, with one farmer confiding that he had never really thought [formally] about the future.

While all farmers identified goals during the research interviews, some farmers developed these on the spot. Distinguishing between goals and dreams was therefore required. The mission statement is the culmination of the individuals’ values and goals, however if these are poorly identified then the task of developing a mission statement is difficult and the tendency was for farmers to leave this for someone else to write, or to ignore it. Of the ten case study farms only four had developed a mission statement: not surprisingly these farms also had clearly defined values and goals.

The level of on-farm analysis was another obstacle and possibly presents one of the biggest challenges to Balanced Scorecard adoption. The level of business assessment by farmers was low. Typical farm business analysis tools were budgets, production monitoring, pasture monitoring and most farmers were involved in book-keeping. Budgets, although prepared were rarely used in conjunction with managing the actual cash flow.

Business success was generally based on the end of year cash balance and level of milk production achieved. Some farms used economic farm surplus (EFS, operating profit or EBIT) however not all farmers who used this measure understood it. Business assessment had a strong operational focus, such as costs and prices. Farmers’ knowledge and understanding of drivers of business performance, financial management and the development and use of performance indicators was low.

Little account was taken of solvency or even debt servicing issues and return on assets or capital was generally not used as a performance measure. With the exception of one farm, there was no substantive long-term financial analysis of business health. This is of concern, but not surprising, as the industry itself focuses on short-term operational measures in its advisory work with farmers (Deane, 1993).

Owner-operators generally have a strong capital base and this creates an environment where poor business and financial management can be hidden for a number of years before it is recognised as a problem, often by outsiders. Four of the case farmers were eroding their net worth but were unaware of this fact because they had inappropriate monitoring systems in place to determine what was happening to this aspect of their business.

In developing strategic objectives with farmers for the Balanced Scorecard, the following observations were made:

The financial perspective was relatively straightforward with goals and indicators being readily identifiable. Most farmers had financial goals. Their ability to identify financial measures appeared to depend directly on the level of financial analysis they had undertaken. Measures identified generally did not cover the whole business and tended to focus on the operational measures related to production and operating profit.

The customer perspective varied in its prominence depending on the farming enterprise. The dairy farmers generally did not consider themselves to have customers or they viewed the dairy company as their customer. Consequently, identifying measures for the customer perspective proved difficult for farmers.

Few considered the importance of having a good relationship with their suppliers for example fertiliser suppliers, veterinarians and bankers. It was difficult to ascertain whether the observed responses to the customer/supplier focus are due to the traditional position of farmers as weak buyers and sellers; alternatively, it may be a reflection of the importance, or lack of, that they place on this issue because they do not understand their position in the supply chain.

In both Australia and New Zealand the role of the customer/consumer in farm business decision making cannot be underestimated. Similarly, the development and value of supplier relationships is often underestimated. On-farm quality assurance systems, contractual arrangements and strategic alliances are examples of initiatives aimed at improving the supplier-customer relationship for the common good.

The internal business perspective was adequately covered in most of the farm business plans. The case farmers were most comfortable working with this aspect of their farm business. A lack of longer-term planning for production was also a weakness of these farmer’s plans

The final perspective, learning and growth, was poorly covered for most of the farms studied. The farmers were not readily able to establish measures that related to their own personal and professional development.

Areas identified for additional training again highlighted the farmers’ production orientation ie. pasture production, cow nutrition, and feed ration balancing. Despite their lack of business management knowledge/skills, the farmers did not appear to see this as a priority area for improvement.

This is consistent with research that suggests that farmers perceive financial management to have a high time input but low benefit. Staff training and management, while acknowledged as important by most of the farmers, rarely had a corresponding formal plan in place to meet this need. Achieving staff success was typically expressed in terms of remuneration, time-off and the relationship with the owner.

The Balanced Scorecard aids strategic management but it can only be used effectively if the basics of preparing strategy are adhered to. This also means that farmers have to identify or understand the link between strategic and tactical management, which in turn requires a shift in farmer and industry perceptions of what success is.

There are several possible reasons why farmers have not adopted strategic planning. It may be prevented because couples have not identified their values, which are essential for goal formulation (Olsson, 1988).

Where farms have clear, well-established values, they are more likely to follow a structured process leading to goal attainment, provided they have business planning knowledge and skills. However, where farms have only vague values they tend not to have formulated goals leading to lax decision making (Olsson, 1988).

Most of the case farms were characterised by vague values and absent goals and had a tactical and operational management focus. Having well defined values, however, does not automatically lead to realistic goals or strategy development. Further goals are often strategic but the management focus is tactical and operational; thus, the appropriate measures for goal attainment are not in place.

The tactical focus may also be influenced by the common belief that high production levels are responsible for a healthy business (Deane, 1993). This is exacerbated by both a community and industry perception, that success is dependent on the quantity of milksolids produced per cow or hectare (Deane, 1993).

These measures are routinely made. Financial information that usually accompanies this data such as operating costs as a percentage of gross farm income and economic farm surplus (EFS) add support to this perception of farm business success. However, as Shadbolt (1998) explained, EFS does not tell the whole story, particularly on whether value is being created by the farm’s activities.

These management foci encourage farmers to accept production based goals with a narrow range of business health indicators. Hence, unless farmers understand strategic management themselves, they are currently unlikely to find much support from within the industry. Further, this situation encourages the majority of farmers to maintain an external locus of control with respect to their personal and business future.

To overcome these barriers to the adoption of strategic management by farmers, its value and importance to their business and future success must be demonstrated and advocated. The use of descriptive planning tools such as a strategy map (Figure 2 and Figure 3 ) may help to break strategic planning into more readily accepted components. The diagram helps to "visualise" the linkages between different parts of the farm business and highlights where lead and lag indicators could be adopted.

The Balanced Scorecard is not a panacea for poor farm business management. It does not replace the need for farmers to have the knowledge on how to identify values and goals, develop a vision and mission statement or analyse the business. Without this foundation knowledge and understanding a Balanced Scorecard that is meaningful to the farmer cannot be developed. The Balanced Scorecard does help farmers to see the linkages that occur within the business and to provide an appreciation of the need for perspectives beyond production and finance.

Bibliography

Birch, C. (1998). Balanced Scorecard Points to Wins for

Small Firms. Australian CPA, 68(6), 43-45. Butler, A., Letza, S. R., and Neale, B. (1997). Linking

the Balanced Scorecard to Strategy. Long Range Planning, 30(2), 242-253. Deane, T. M. (1993). The Relationship Between Milkfat

Production Per Hectare and Economic Farm Surplus on New Zealand Dairy Farms. The

Proceedings of the New Zealand Society of Animal Production., 53, 51-53. Gubman, E. L. (1998). The Talent Solution: Aligning

Strategy and People to Achieve Extraordinary Results. New York: McGraw-Hill. Kaplan, R. S. and Norton, D. P. (1992). The Balanced

Scorecard - Measures That Drive Performance. Harvard Business Review,

(Jan-Feb), 71-79. Kaplan, R. S. and Norton, D. P. (1996a). Knowing the

Score. Financial Executive, (Nov-Dec), 30-33. Kaplan, R. S., & Norton, D. P. (1996c). The

Balanced Scorecard: Translating Strategy into Action. Boston, Massachusetts:

Harvard Business School Press. McCann, M. (2000). Turning Vision Into Reality. Management

Accounting, 78(1), 36-37. Newing, R. (1995). Wake Up to the Balanced Scorecard. Management

Accounting, (March), 22-23. Olsson, R. (1988). Management for Success in Modern

Agriculture. European Review of Agricultural Economics, 15, 239-259. Parker, W.J. (2000a). Principles of Successful Business

Management. Proceedings of the Large Herds Conference, Christchurch New Zealand,

March. Parker, W.J. (2000b). Farm performance measurement -

linking monitoring to business strategy. Proc. NZ Society of Animal

Production. 59: 6-13. Rawlings, K.M. (1999). Key Performance Indicators for Goal

Attainment in Dairy Farming: Essential Elements for Monitoring Farm Business

Performance. Unpublished Masters Thesis, Massey University, Palmerston North,

New Zealand. Robbins, B., & Wallace, D. (1992). The Family

Business: How to successfully manage a Family Business. Melbourne,

Australia: The Business Library. Shadbolt, N. M. (1998a). Benchmarking Dairy Farm

Businesses. Large Herds Australia Conference Proceedings Barossa Valley,

South Australia, March. McMillan College, The University of Melbourne. Towle, G. (2000). The Balanced Scorecard: Not Just Another

Fad. Executive Journal, 40(1), 12-15. Willyerd, K. A. (1997). Balancing Your Evaluation Act. Training,

(March), 52-58.

![]()